In Jay B. Barney’s text Gaining and Sustaining a Competitive Advantage, he describes the valuation of a target firm, and notes that this value depends on the combined value of the two firms as illustrated by the following equation:

P = NPV(A+B) – NPV(A)

He goes on to discuss how a bidding war will ensure efficient pricing of the target firm, but here is where I think we should again point out that the value of the acquisition is derived from the combined value of the two entities; therefore, it is possible (and likely) that different acquiring firms will have differing valuations of a target firm because the sum of their parts may create different revenue opportunities that do not exist with other firm combinations.

Tesla acquired SolarCity in 2016, saying that “the combination would create the world’s first vertically integrated sustainable energy company, taking advantage of the synergies created by linking Tesla’s energy storage with SolarCity’s solar generation.” In 2019, Tesla acquired Maxwell Technologies, a manufacturer of energy storage and power delivery using ultracapacitors. Musk posits that ultracapacitors will be key in advancing battery technology and performance in EVs and that acquiring a company to produce battery technology in house will create cost efficiencies that will reduce the cost of their EVs. These acquisitions are both examples of:

- a vertical merger, in which a firm acquires a supplier

- a product extension merger, in which a firm gains access to complementary products, and;

- a market extension merger, in which a firm gains access complementary markets.

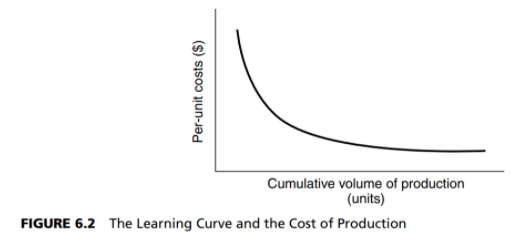

Tesla uses the strategy of vertical integration and narrow diversification in related businesses to create cost efficiencies and value for shareholders, investing in technologies to advance its core business of manufacturing and selling EVs.